Companies that commit to tracking and publicly disclosing their sustainability performance can improve their environmental, social, and governance (ESG) performance while also earning rewards from clients and investors.

Introduced by the European Commission in 2022, the Corporate Sustainability Reporting Directive (CSRD) sets the benchmark for approximately 50,000 EU companies to report on their environmental impact.

The directive will replace and expand on the Non-Financial Reporting Directive (NFRD) by providing more specific reporting requirements and increasing the number of enterprises required to comply.

What is the CSRD, which companies does it impact, and can it affect your business? Keep reading this in-depth CSRD explainer to find out.

What is the CSRD?

The CSRD is a European Union (EU) law that took effect on January 5, 2023, and compels EU organisations to report their environmental and social impacts, as well as how their environmental, social, and governance (ESG) efforts influence their business.

The directive applies to qualified EU subsidiaries of non-EU corporations as well. This means that a US-based corporation with multiple subsidiaries must comply with the CSRD even if only one of its subsidiaries is located in the EU.

The CSRD’s purpose is to offer clarity to investors, analysts, customers, and other stakeholders so that they can better evaluate a company’s sustainability performance, as well as the associated business implications and risks. This covers a number of general business metrics that are not covered as part of direct financial reporting.

Introduced as part of the European Commission’s Sustainable Finance Package, the CSRD broadens the scope, sustainability disclosures, and reporting obligations of its predecessor, the Non-Financial Reporting Directive (NFRD).

What does the CSRD mean for businesses?

The CSRD compels organisations to disclose information on how their business activities influence the environment and people, as well as how their sustainability objectives, metrics, and risks affect the company’s financial health. This also includes a number of primary and secondary financial KPIs.

For example, CSRD requires an organisation to report not only its energy usage and costs but also emissions metrics that detail how that energy use impacts the environment, targets for reducing that impact, and insights into how meeting those targets will affect the organisation’s finances. This includes impacts on metrics like cash flow, liquidity, etc.

All CSRD disclosures must be made public, and third-party auditing is required to ensure their correctness and completeness.

Why was the CSRD introduced?

The EU believes that consumers and investors should be aware of a company’s sustainability effects, and the CSRD was adopted because previous regulation was inadequate.

Before the CSRD, the Non-Financial Reporting Directive (NFRD) defined reporting rules for large enterprises. However, the European Commission found that the submitted information was insufficient. Here are the most important goals of the CSRD:

Focus on double materiality

The CSRD, like the NFRD, demands “double materiality,” which implies that corporations must report not just the risks they face from climate change but also the potential consequences to the environment and society.

Increasing transparency for investors

According to the European Commission, low-quality sustainability reporting can have cascading repercussions, particularly when it comes to supporting sustainable investments. To guarantee the credibility of the green investment market, investors must understand the sustainability consequences of their investment portfolio.

Even investors who are not especially inclined to engage in green enterprises must comply with the Sustainable Finance Disclosure Regulation (SFDR).

The CSRD was established with the purpose of increasing transparency and giving investors the information they need to assess a company’s sustainability.

Reporting standardisation

The CSRD will force companies to report sustainability data in a standardised digital format. This is intended to establish a clear standard for firm sustainability reporting, which is now plagued with idiosyncratic forms, allowing for greater understanding and easier comparison among organisations.

The CSRD was designed to also put a stop to greenwashing, improve the EU’s social market economy, and establish the framework for worldwide sustainability reporting requirements.

Key areas of impact of the CSRD directive

The CSRD is expected to have a wide-ranging impact, including improving the comparability of sustainability reporting, affecting especially the following areas:

- Reduced cost of sustainability reporting: The CSRD is expected to clarify and offer certainty regarding the sustainability information that must be reported, making it easier to gather information from business partners such as suppliers, clients, and investee firms. Furthermore, it is intended to reduce the requests organisations get for sustainability information.

- Reduced systemic risks to the economy: More full disclosures are projected to enhance the allocation of financial capital to enterprises and projects addressing social, health, and environmental challenges.

- Global coverage and standardisation of sustainability reporting standards: The ESRS was created by leveraging and merging existing standards and frameworks, including the Task Force on Climate-related Financial Disclosures (TCFD) and the Global Reporting Initiative (GRI). This is not just a significant milestone for the EU, but a key contribution to worldwide reporting standardisation efforts.

Does the CSRD apply to your company?

The CSRD quadruples the number of enterprises obliged to report on sustainability, from 11,000 in the NFRD to over 50,000 under the CSRD. By 2028, all of the following companies or enterprises must comply with the CSRD:

Companies listed on an EU-regulated market exchange

The exception are “micro undertakings” that fail to fulfill two of the following three requirements on successive balance sheet dates:

- At least EUR 450,000 in total assets.

- At least EUR 900,000 of net turnover (sales).

- At least ten employees (average) throughout the year.

EU-based large enterprises, listed or not

The directive also applied to any public or non-listed corporations that fulfill two of the following three requirements on any two consecutive balance sheet dates:

- At least EUR 25 million in total assets.

- EUR 50 million in net turnover.

- An average of 250 employees each year.

“Third-country” initiatives

These are non-EU parent firms with annual EU revenues of at least EUR 150 million in the last two years, and they also own:

- A large EU-based activity.

- An EU-based subsidiary whose securities are listed on an EU-regulated market exchange.

- An EU branch office with at least EUR 40 million in net revenue.

When must companies comply with the CSRD?

CSRD compliance is being phased in from 2024 to 2029. It’s mostly dependent on NFRD heritage or company size.

Here are several important milestones included in the directive:

- Fiscal year 2024 (reporting in 2025): Compliance is mandatory for companies (or ‘entities’) that are already required to comply with the NFRD. This applies to all organisations listed in an EU-regulated market with 500 or more workers.

- Fiscal year 2025 (reporting in 2026): Compliance is mandatory for large undertakings that haven’t already been required to comply with the NFRD.

- Fiscal year 2026 (reporting in 2027): Compliance is required for small and medium-sized enterprises (SMEs) listed on an EU-regulated market.

- Fiscal year 2028 (reporting 2029): Compliance is required for some third-country projects.

Reporting on sustainability: ESRS

In 2022, the European Financial Reporting Advisory Group (EFRAG) published the first set of European Sustainability Reporting Standards (ESRS).

The ESRS defines the metrics that organisations must report and how to submit them in order to comply with CSRD disclosure obligations.

There are 13 ESRS detailing disclosures and data spanning sustainability issues across four categories:

- Cross-cutting: (ESRS 1) General principles; (ESRS 2) General, strategy, governance, and materiality assessment.

- Environment: (ESRS E1) Climate change; (ESRS E2) Pollution; (ESRS E3) Water and marine resources; (ESRS E4) Biodiversity; (ESRS E5) Resource use and circular economy.

- Social: (ESRS S1) Own workforce; (ESRS S2) Workers in the value chain; (ESRS S3) Affected communities; (ESRS S4) Consumers and end-users.

- Governance: (ESRS G1) Governance, risk management, and internal control; (ESRS G2) Business conduct.

All organisations covered by the CSRD are expected to report on Cross-cutting issues, whereas ESG reporting is required for those deemed relevant.

The European Union’s institutions decided in February 2024 to push back the date for implementing sector-specific European Sustainability Reporting Standards (ESRS) by two years. Sector-specific ESRS are projected to be produced by June 2026, leaving the CSRD effective dates unchanged.

Who sets the CSRD reporting standards?

EFRAG, a private group principally funded by the EU, assists the European Commission on adopting worldwide reporting standards for EU law. EFRAG is in charge of the new directive standards on behalf of the European Commission.

To accomplish that, EFRAG works with numerous entities to provide technical guidance, including:

- The European Banking Authority

- The European Environmental Agency

- The European Insurance and Occupational Pensions Authority

- The European Securities and Markets Authority

The goal of this partnership is to guarantee that the CSRD standards are consistent with EU regulations.

As soon as the standards are established, EFRAG provides enterprises with particular reporting requirements under the ESRS. To increase stakeholder accessibility, companies must collect this information and provide disclosures in management reports.

Companies must submit an annual report in the European Single Electronic Format (ESEF) and digitally tag information with iXBRL to make it machine-readable for use in the European Single Access Point.

Note that the CSRD requires a third party to audit and verify the sustainability facts and statistics in the report. Initially, compliance requires the auditor to give minimal assurance, primarily based on the organisation’s representations.

However, during the following three years, the CSRD will need reasonable certainty, based on the auditor’s inspection and knowledge of the organisation’s activities, procedures, and controls.

How can companies comply with the CSRD?

To comply with the CSRD, businesses must acquire and combine massive amounts of data. A robust ESG data foundation may assist ease reporting, make CSRD disclosures auditable, and better prepare firms for the reforms that will take effect in 2024.

What happens to companies that fail to comply with the CSRD?

The CSRD mandates EU member states to establish an investigation and compliance organisation to administer effective, appropriate, and dissuasive sanctions. These fines depend on many factors, including the severity and duration of the breach, as well as the company’s financial status.

Individual member states set CSRD noncompliance sanctions based on applicable state legislation. Every corporation should remain up to speed on legislative changes and get legal counsel to guarantee compliance and prevent inquiries and potential penalties.

How to prepare for CSRD?

Here are a few key steps companies should take to prepare for CSRD:

- Create and prepare a twofold materiality evaluation – To conduct the double materiality evaluation, all stakeholders and levels of the value chain must be reviewed, and the assessment should take into account the immediate, medium, and long-term effects of the company’ activities.

- Familiarise yourself with the European Sustainability Reporting requirements (ESRSs) for enterprises affected by the CSRD – Businesses will be expected to achieve these standards, so having a good grasp of the regulations is essential.

- Gather and monitor data – Businesses must gather data from their own operations, suppliers, and business partners before include it in their sustainability reports. For the first time, the CSRD will implement an EU-wide audit (assurance) requirement for ESG information. As a result, CSRD-impacted enterprises will be obliged to do due diligence and audits on their operations, including reporting on scopes 1, 2, and 3 of their carbon emissions.

- Align risk management with the company’s sustainability plan – Businesses that engage completely with sustainability risk factors from the start will be able to better connect their activities with sustainability, business value, and risk mitigation measures.

- Integrate reporting – To guarantee that the overall management report that CSRD-affected firms must produce is transparent and effective, use a solid reporting framework to go above the minimum criteria for presenting their sustainability performance.

- Comply voluntarily – Compliance with such standards on a voluntary basis is a critical step towards not just preparing for the CSRD, but also effectively incorporating sustainability into overall company processes.

Reporting on sustainability in the UK: What is the UK SDS?

With a planned release in July 2024, the UK Sustainability Disclosure Standards (SDS) establish corporate disclosures on sustainability-related risks and opportunities that businesses face.

The SDS will form the basis of any future obligations in UK legislation or regulation for corporations to report on risks and opportunities related to sustainability issues, including risks and opportunities stemming from climate change.

The new UK SDS will be issued in the UK by July 2024, with an effective date of January 1, 2025. The UK Department for Business and Trade will publish SDS based on the IFRS® Sustainability Disclosure Standards produced by the International Sustainability Standards Board .

Following the development and release of the UK SDS, the standards will be included in legal and regulatory reporting obligations for UK organisations. Using the ISSB standards as a baseline, the goal is to assist UK companies in disclosing internationally consistent sustainability information to investors, regulators, and other capital market players.

Currently, there are no specific statutory or required reporting obligations for major or publicly traded UK enterprises to report under the UK SDS. However, given the ISSB’s predicted international acceptance and the existence of current UK sustainability reporting obligations under SECR and the FCA, it’s reasonable to expect FCA and SECR-eligible corporations to explore adopting the ISSB standards in advance of the UK SDS.

While SDS is yet to be finalised and officially adopted, it’s expected to become an authoritative UK sustainability reporting standard.

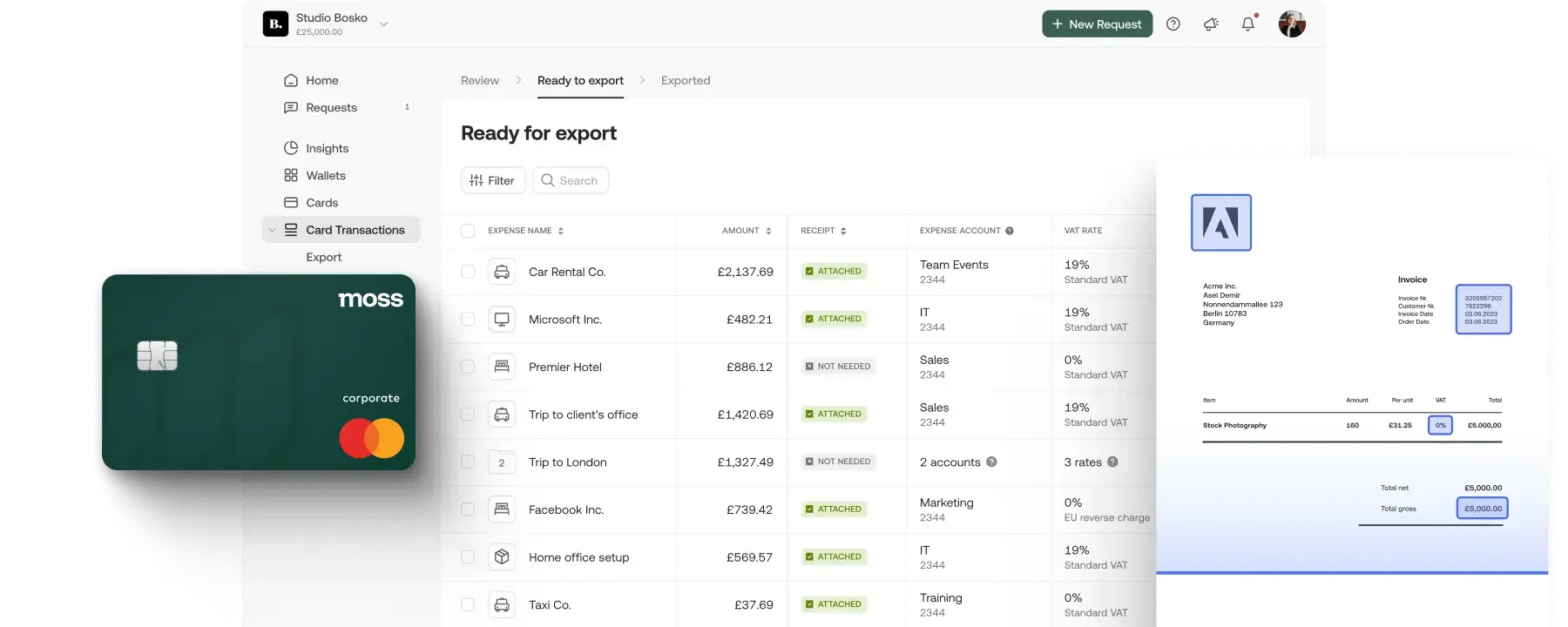

Managing spend with Moss

While the CSRD is certainly helpful to stakeholders and the environment, its comprehensive breadth and unparalleled depth are bound to become challenging for many organisations. The twofold materiality concept at the heart of the CSRD will have a significant impact on the type and methods organisations will use to gather sustainability data. Despite the anticipated hurdles, the CSRD will open up new opportunities for businesses to incorporate sustainability into their operations.

While the CSRD is primarily related to non-financial business metrics, financial data plays a key role in determining many of the environmental and sustainability related metrics that will be included in the ESRS.

At Moss we help businesses take control of their spend with smart corporate credit cards and a suite of tools to manage everything from accounts payable automation to employee expense reimbursements. Spend activity that happens via Moss is recorded and used to develop valuable financial insights for controlling and FP&A. All of your spend data can then be fed directly to accounting software for financial reporting, and in turn be used for secondary KPIs and reporting metrics related to the CSRD.